Reverse Charge Mechanism

Introduction – Reverse Charge Mechanism in UAE VAT

Reverse Charge Mechanism is a process under which responsibility of paying tax to Government shifts from seller to buyer, unlike in the forward charge, where the supplier is liable to pay the tax. This mechanism of reverse charges applies on the import of goods and services into UAE. The whole process revolves around the receiver or the recipient of the goods and services.It is the importer or the receiver of goods and services who pays tax to the Government.

Knowledge gained from the post

- Why Reverse Charge Mechanism is required in UAE?

- Goods covered under Reverse Charge Mechanism VAT in UAE

- Exception to the Rule

- Understanding Reverse Charge Mechanism with Examples

- Responsibilities of Importer of Goods and Services under Reverse Charge Mechanism of UAE VAT.

- Accounting Entries for Reverse Charge Mechanism(RCM) in UAE

- Treatment of Reverse Charge Mechanism in filing VAT Returns process in UAE

- Reach Accountant Online VAT Accounting Software assistance provided for VAT under Reverse Charge Mechanism.

Why Reverse Charge Mechanism is required in UAE?

The concept of Reverse Charge Mechanism has been incorporated in UAE as to ensure there is no kind of tax evasion on any goods or services. The supplier is not a taxable person in UAE and the supply has been made in the state of UAE Therefore to account for the taxes of the goods or services received ,the recipient or the buyer is treated as a person making taxable supplies to himself and will be responsible to pay VAT to the government. The reverse charge mechanism is mainly used for cross-border transactions. Since a seller does not have business in UAE, it will be difficult for the tax authorities to track these sellers or suppliers. Hence, buyers who are residents of UAE are made responsible to charge VAT on reverse charge basis.Reverse Charge Mechanism eliminates the obligation for the overseas seller to register for VAT in the UAE.Reverse charge is only applicable if purchases are made outside the UAE. Therefore It relieves non-resident suppliers of the burden of registering and accounting for VAT in their buyers’ location.

Goods covered under Reverse Charge Mechanism VAT in UAE

Import of concerned goods or services and supply of any crude or refined oil, unprocessed or processed natural gas, or any hydrocarbons for resale or to produce and distribute any form of energy are under reverse charge VAT. The UAE VAT Law has listed the following supplies liable for VAT on reverse charge mechanism in UAE, provided the conditions are fulfilled as prescribed in UAE Executive Regulations:

- Imports of concerned goods or concerned services for business purpose

- Taxable supply of any crude or refined oil, unprocessed or processed natural gas, or any hydrocarbons for resale or to produce and distribute any form of energy by registered supplier to registered buyer in the State of UAE

- Supply of goods or services by a supplier who does not have a place of residence in the state to a taxable person who has a place of residence in the State of UAE.

Recipient is liable for Reverse charge mechanism on the applicability of the above mentioned supplies and conditions. However, for each of the above supplies, specific conditions are mentioned in the UAE VAT Executive Regulations which need to be full filled, to be liable for reverse charge VAT.

Exception to the Rule

When the goods are imported with the intention of exporting to another GCC state, then the importer must pay import VAT and cannot claim the input VAT. Here the reverse charge mechanism does not apply.

Where goods are imported into the UAE (i.e. released for consumption here)but the intention is that these goods will be transferred by theimporter into another GCC State, the place of supply of import shall be UAE, However:

- The importer must pay import VAT without using the reverse charge and cannot recover this VAT.

- This import VAT should be recoverable in the GCC State to which the goods are transferred.

Understanding Reverse Charge Mechanism with Examples

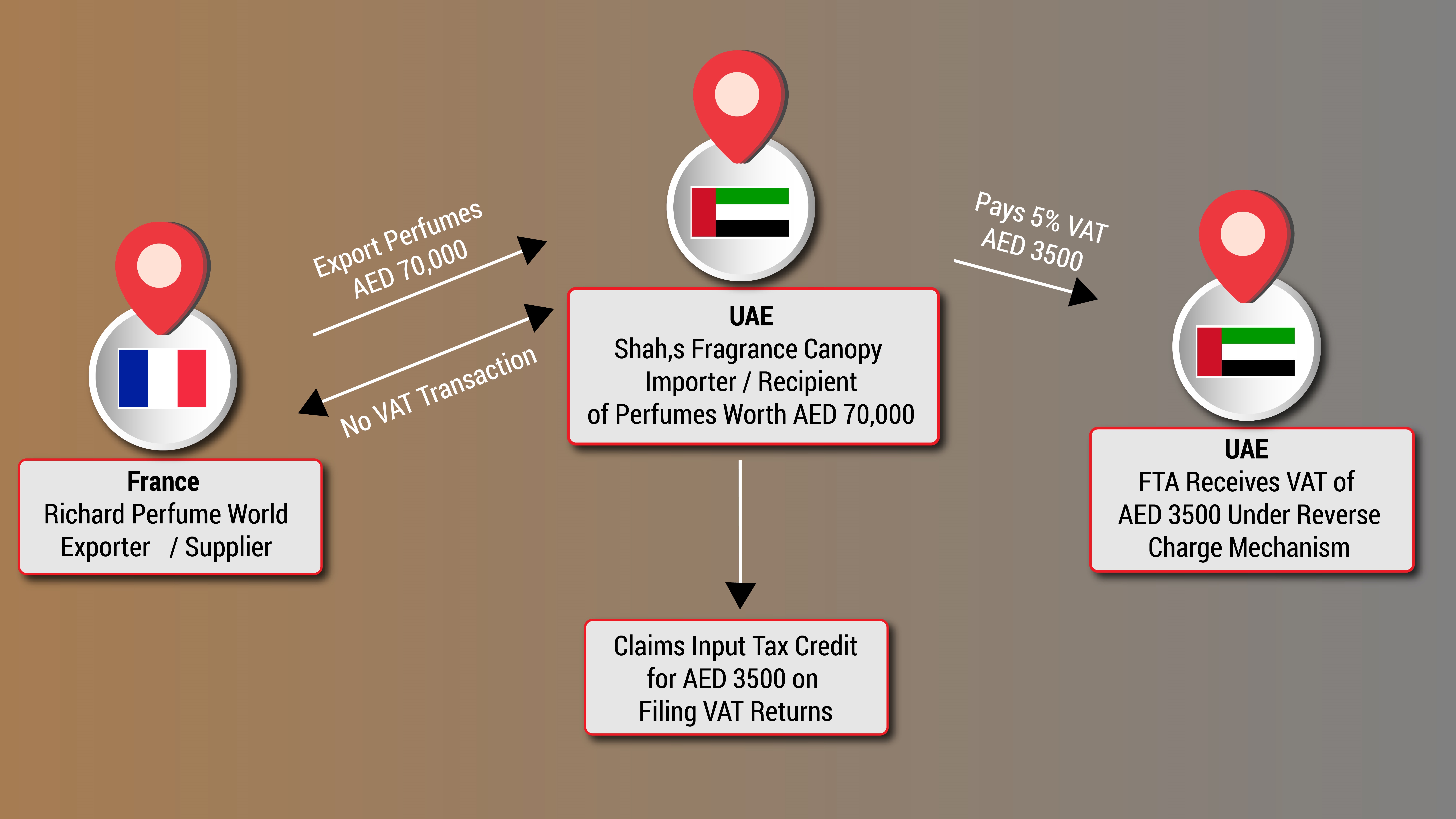

Scenario:1

Richards Perfume World a company in France exports perfumes referred as supplier or exporter worth AED 70,000 to Shah’s Fragrance Canopy in UAE referred to as recipients or receiver of the goods.

Richards Perfume World is not VAT registered in UAE therefore not required to pay taxes.

Shah’s Fragrance Canopy is a registered entity in UAE. As being registered importer, Shah’s Fragrance Canopy is liable to pay VAT @5% on AED 70,000 to the Government .VAT under reverse charge mechanism is AED 3500 /-

The buyer will reports the Input VAT (VAT on purchases) as well as the output VAT (VAT on sales) in their VAT return for same quarter. This means Shah’s Fragrance Canopy claims AED 3500 as Input Tax which can be adjusted against output tax payable.

The most used way of setting up the reverse charge mechanism is to use Offset Tax. This works by creating a tax with the type of ‘Offset’. You can also set your reverse charge taxes up by using the ‘Self Assessed.

Scenario 2: If the business owner in the State is a non-registered person for VAT, then VAT would be paid on goods being imported from outside the GCC. Such VAT will typically be paid before the goods are released to the person.

Example: Saif is a non-registered business owner under VAT in the UAE. He imports goods from places outside the GCC. In this scenario, VAT is due to the UAE government and has to be paid before the goods are released to Saif.

Scenario 3: If goods are transhipped via UAE to other GCC countries, import VAT is applicable. The Input Tax Credit cannot be claimed in UAE, but can be claimed in the final destination member state.

Example: Khan deals in accessories, and he tranships goods via the UAE to other GCC countries. In this case, import VAT is applicable. Although Khan has to pay VAT in the UAE, the input tax credit cannot be claimed there. He can only claim it in the destination state.

Scenario4: If Goods are previously imported to UAE and then exported to other GCC countries, import VAT is applicable. The input credit recovered via reverse charge has to be paid back to the UAE tax authority.

Example: Shaan owns an electronics business in the UAE and Kuwait. He previously imported 100 television sets to the UAE, and then he exported 40 of them to Kuwait (which is also a GCC country). In this case, the input tax credit which Shaan received on the 40 television sets has to be paid back to the UAE tax authority.

Responsibilities of Importer of Goods and Services under Reverse Charge Mechanism of UAE VAT.

- The receiver of the goods or services must be registered for VAT.

- Determine the value on which tax needs to be levied

- Account the VAT due on reverse charge supplies

- Remit VAT to the government

- Claim Input Tax, if eligible.

- Maintain the records such as invoice and other documents to substantiate the tax payment and input tax claim

- Invoices, receipt vouchers, and refund vouchers should all specify whether the tax payable for that particular transaction is through reverse charge

Accounting Entries for Reverse Charge Mechanism(RCM) in UAE

| S.No | Particulars | Debit | Credit |

| 1. | Purchase A/C & Expense A/c | xxxx | |

| Input Vat -RCM A/C | xxxx | ||

| To Bank Creditors A/C | xxxx | ||

| To Vat payable RCM a/c | xxxx | ||

| 2 | For Sales: | ||

| Bank / Debtor A/C | xxx | ||

| To Sales A/C | xxx | ||

| To Output Vat A/C | xxx | ||

| 3. | Quarterly/Monthly Journal for VAT Payment | ||

| Output Vat A/C | xxx | ||

| Vat payable RCM a/c | xxx | ||

| To Input Vat RCM A/C | xxx | ||

| To Vat Payable A/C | xxx | ||

| 4. | Payment to FTA | ||

| Vat Payable A/C | xxx | ||

| To Bank A/C | Xxx | ||

| 5. | Quarterly / Monthly Journal for VAT Refund | ||

| Vat Refund A/C | Xxxx | ||

| Output Vat A/C | Xxx | ||

| Vat payable RCM a/c | Xxx | ||

| To Input Vat RCM A/C | Xxx | ||

| 6. | Refund received from FTA | ||

| Bank A/C | Xxx | ||

| To Vat Refund A/C | xxxx |

Treatment of Reverse Charge Mechanism in filing VAT Returns process in UAE

Supplies subject to the reverse charge provisions.

The value of supplies of goods and services under Reverse Charge Mechanism should be declared separately. The value of goods imported into UAE will be auto-generated to the extend it was declared under the Taxable Person’s customs registration number.

Goods imported through UAE customs will be reported under Goods imported into the UAE header. In this step services which are imported during the period will be included. For example, if the company has received a service from a software firm located outside UAE worth AED 100,000/-, 5% VAT i.e. AED 5,000/- will be shown as Output VAT under this step. However, the same amount can be taken as input under Supplies subject to the reverse charge provisions header provided other provisions of the law is met. Any expenses where VAT is incurred and falling under Reverse Charge Mechanism for which Input Tax is not recoverable, those expenses should not be stated. If you have paid VAT during import due to any reason, such VAT amount can be mentioned for reimbursement.

It can be seen the ultimate effect of reverse charge mechanism is same as forward charge .The only difference in reverse charge VAT is the shift in the responsibility of paying VAT which is moved from supplier to the recipient .Therefore Government of UAE have also made provisions to claim refund on Reverse charge VAT promoting international transaction with ease to the importers.

Conclusion

One of the key steps in being VAT compliant is choosing the right VAT software matching all your business requirements. Reach Accountant software is well designed to match all the needs for successful running of the business. The software can be used in different industries ,traders ,manufacturers, retailers, workshop ,business projects etc. It is an accounting software that can automatically manage your book of accounts, taxes, inventory, sales, purchases and more online quickly and securely.

Popular posts

Related Blogs